Lending and the Engineering of Chaos

Dynamical Systems and the Fight to Conquer Entropy

A bank’s attitude to risk is not passive and defensive; a bank actively and willingly takes on risk, because it seeks a return and this does not come without risk. Indeed risk management can be seen as the core competence of a bank.

-Alexander J. McNeil, Rüdiger Frey, & Paul Embrechts, Quantitative Risk Management

A Brief History of Chaos

In 1961, the prolific engineer and meteorologist Edward Lorenz pioneered modern Chaos Theory1, originally named “Sensitive Dependence on Initial Conditions”, while simulating sequences of water molecules to predict weather patterns.

Lorenz discovered that the predictions of his deterministic simulations were extremely sensitive to minuscule changes in the initial conditions. The profound consequence being the realization that some systems in nature are unfathomably volatile.

This, too, is true of the quantification of risk.

Borrowing Short to Lend Long

In the wake of Silicon Valley Bank’s collapse, there’s been much attention on how banks “borrow short to lend long”, while this is true the important details are in how they lend long.

The "how" dictates a banks very survival and while there is variance across banks I’d bucket them into two categories:

Manual

Algorithmic

Alex Johnson nicely characterizes the first as “Relationship Lending”, which served humans for most of our existence until Discover, Capital One, and a handful of others shook the finance industry with automation in the 1990s.

In recent decades, Fintech enhanced this approach further through advances in software and quantitative underwriting—all in the service of increasing conversion2.

Lending

To be a little reductionist, lending reduces to: a decision, a price, and a duration.

At a high level, these three things rely on answers to four important questions

How much does it cost to lend?

What’s the maximum you are allowed to charge?

Can this person or entity pay you back?

Will this person or entity pay you back?

There are many important details like how these things evolve over time, how price sensitive a consumer is, how the price impacts whether the consumer can afford the loan, how the duration of the loan impacts the risk, and maybe even some consideration for the cost of acquisition, but this gross simplification provides a nice starting point.

So how do we get answers to our questions?

The Fed

State and Federal regulations

Data and math

More data and more math

The first two are reasonable, we look at the interest we give to our deposit customers and any interest rate we charge above that for our loans is expected profit (minus some other stuff).

The latter two is where the competition begins.

Financial Data is Beautiful Chaos

In a previous article discussing Fintech and machine learning, I stated that “Financial Data is Chaos” and outlined why. In short, “everything surrounding this money stuff was kind of made up by humans to keep track of things. That is a profoundly different phenomenon than your visual cortex, linguistics, or the laws of physics.”

Financial data is more than just data.

You are observing real people with real lives, and real life is beautiful chaos.

We fall in love, get our first car, go off to college, move away from home, get married, grow our families, say goodbye to loved ones, and sometimes even buy a home—and all along the way the financing of our purchases with money stuff is an annoying detail we sometimes have to think about.

Crude representations of all of that life are stored in a bunch of stupid databases that banks use to try and make reasonable business decisions about whether or not we can afford to pay for those things on some schedule.

All of that life—encoded in data—is what makes modeling risk so fascinating…and also terribly complicated.

So how, then, do we do something useful with all of this chaos?

Lending is a Math Puzzle

In the aforementioned article where I was focusing on discussing Artificial Intelligence and Fintech I also stated that “consumer finance is basically a multivariate constrained stochastic optimization problem.” and lending is actually what I was referring to.

To be explicit, we have data (i.e., a random process), the 4 questions I mentioned above (i.e., variables and constraints), and something we want to optimize (lifetime value of a customer, profit, or maybe something else). In order to solve this optimization problem we need two things:

An underwriting model

Really good engineering that enables (1).

What does that look like?

Underwriting and the Fight to Conquer Entropy

In banking, underwriting is the detailed credit analysis preceding the granting of a loan, based on credit information furnished by the borrower…Of late, the discourse on underwriting has been dominated by the advent of machine learning in this space. These profound technological innovations are altering the way traditional underwriting scorecards have been built, and are displacing human underwriters with automation.

In the modern world, we use data, statistics, machine learning, and software engineering to do credit analysis.

This is what I’ve spent a significant share of the last ten years doing. I’ve worked at AIG, the Commonwealth Bank of Australia, and Goldman Sachs building risk models for commercial and consumer underwriting (among other things) and I can confidently tell you that over that decade, while the questions remained the same, how we approached answering them changed dramatically.

Underwriting (i.e., the approach) has two components:

A risk model

A policy.

What does a risk model look like?

For credit risk models, this equation just says that the probability of Y (maybe previous defaults or delinquencies) depends on some information X (a bunch of features/attributes that may be useful in predicting Y) and the thing on the right is just an old fashion Logistic regression. A logistic regression is a classic approach and while modern-day practitioners may swap the gibberish with something a little fancier (e.g., a machine learning algorithm) it has served banks well for quite a long time.

Note: Mathematically, the Logistic regression solution is a maximum entropy solution and minimizes the cross-entropy loss function. So when I say the “fight to conquer entropy” I’m making a play on words that underwriting is about building good regression models because it is…and it’s a fun math pun3 (*winks*).

I won’t go into the details of how to build a credit risk model but suffice it to say there’s a lot to it. McKinsey has some opinions (lol).

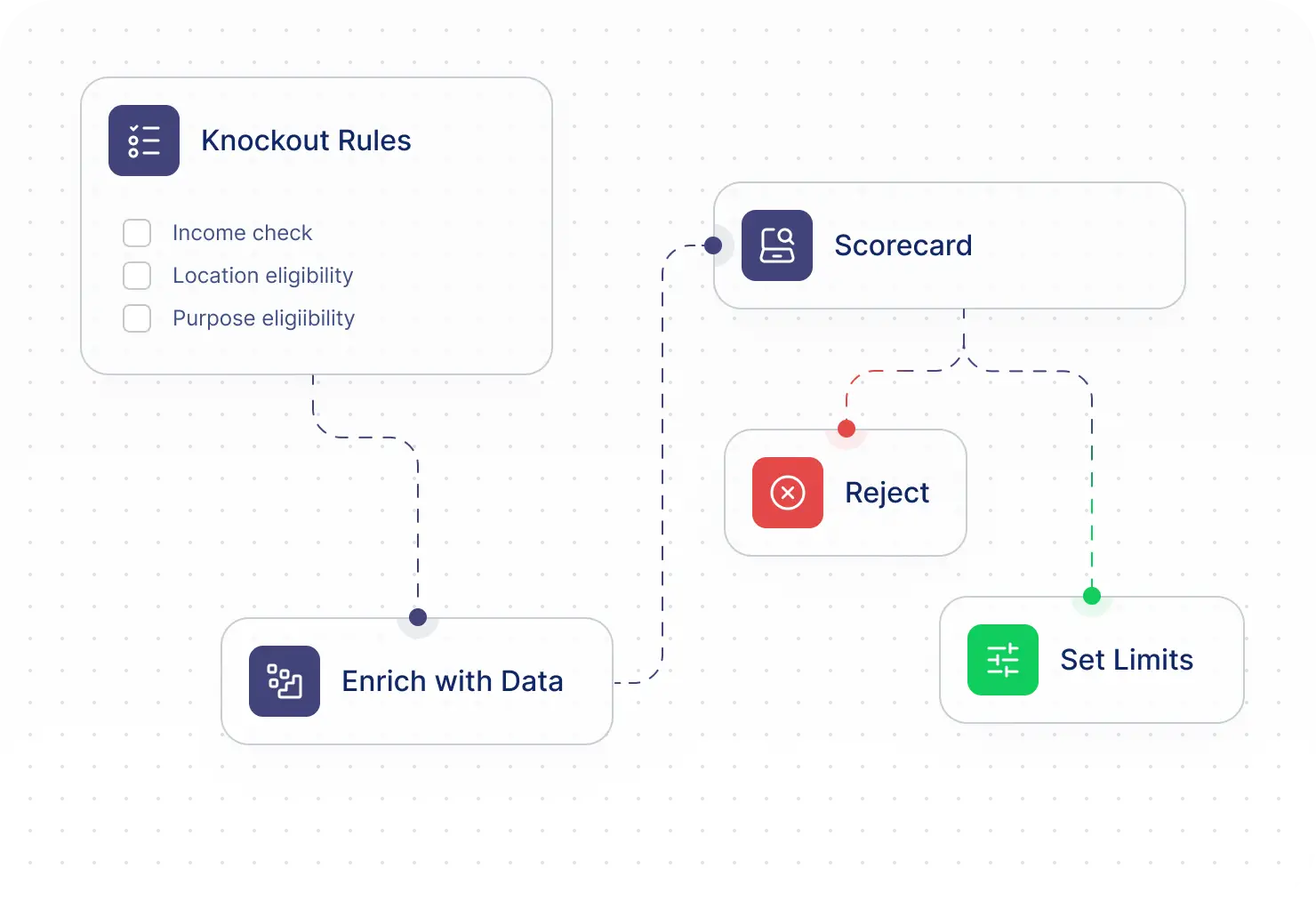

What does a policy look like?

In the diagram above we see rules, data, a scorecard, and a decision (the “Reject” or “Set “Limits”). All key ingredients for underwriting.

But the simple model and the policy above are two trivializations. In the real world this gets more complicated and the rules in a policy spiral into anarchy as different teams look to hit often competing KPIs and these simple rules need their own system.

Cue the Rules Engine.

Rules Engines and the Engineering of Chaos

I wrote before about Fintech and the Anarchy of Rules where I stated that “Rules/Decision engines are ubiquitous” in Fintech.

They codify the world's regulatory policies, represent the risk appetites of banks, and encapsulate the hopes and dreams of analysts grappling with an existential crisis.

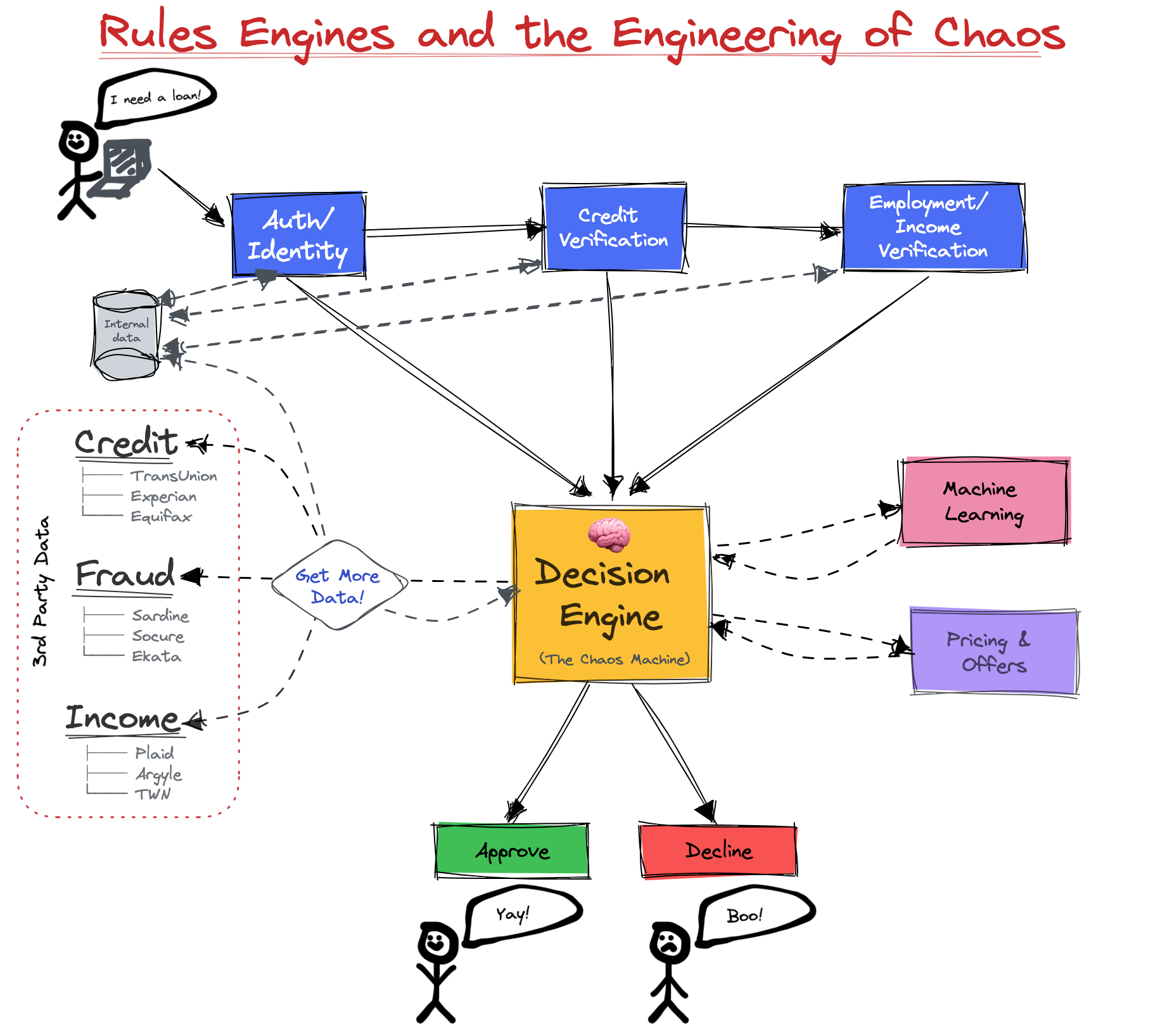

More seriously though, a “Rules Engine” is software that quite literally executes rules4 to make a decision about something and they’re an important piece of software in an overall complicated architecture necessary to handle risk problems at scale.

Note: I know these systems quite well. I’ve worked with too many of them: GDS Link, Provenir, FICO (yes, they offer a decision engine), Sliderule, and I even wrote one myself (🥲). I often get asked “Should I buy or build?” and, in general, I’d say that it really depends on your organization and goals.

In practice, decision engines can have thousands of rules, elaborate decision paths, complex flows of data (e.g., calling TU for some customers and Equifax for others), and an intricate coupling with machine learning models. In the diagram above, I’ve outlined the key components used in the architecture of a decision engine, probably.

This diagram is useless5.

All of the magic (i.e., hard work) is in the code that powers this Chaos Machine6, and I want to explicitly over-communicate that a silly diagram is useful for intuition but it is not useful for anything beyond that. In fact, it is so useless that I happily share it here because there is nothing special about diagrams. There is, on the other hand, a lot that is special about good code. Few companies produce that.

Why do I say this? Because pretty much every bank or lender is doing a version of this diagram. So where does the differentiation happen?

Distribution, Product, and Speed…and also how you do the thing!7

In lending, the how is in the data generation, policy development, machine learning, and the software around the money stuff.

So if you want to build a lending business that compounds over time, you have to be executing well on all of these areas—that’s how Capital One became the Goliath it is today.

Note: I would be remiss if I didn’t mention that once a bank has a portfolio of loans and other financial assets generating liquidity over different time horizons there’s still lots of quantitative work to do and while Basel II provides guidelines for the calculation of minimum capital requirements based on risk weighted assets, managing your capital and liquidity expectations is both a challenging and interesting area of work at a bank.

Closing Thoughts

The optimal amount of fraud is non-zero8.

The banking industry has come a long way since relationship based lending, but there is still ample opportunity for innovation. In the modern world, all of that innovation is driven by software, analytics, and machine learning that reinforces the value of that software.

Lending is the business of losing money and, ultimately, effective risk management means recognizing that the optimal amount of losses is non-zero, indeed.

How you diligently manage those losses is what separates the good lenders from the bad and the best way to control that chaos is through great software.

There are no shortcuts. No single tool will fix brittle and broken systems, so my advice is simple: fall in line or fall by the wayside. The future of money depends on it.

Happy lending! 🏦💸

-Francisco

Some Content Recommendations

Ron Shevlin wrote a great take on the numerous bad takes from Twitter on the SVB collapse.

Jason Mikula wrote an excellent review of Hindenburg's research report on Block. He also wrote about BNPL (where I, of course, have biases). As always, Jason was very thoughtful in his writing. He wrote a lot but I will only share a few thoughts that I have: (1) survey data, while useful, is never as good as measuring actual behavior (what people say they do and what people actually do is, unfortunately, often inconsistent) so the data should be taken with a grain of salt; (2) to quote Jason, “One thing the report does demonstrate is that consumers who choose to use BNPL are heavily indebted across a variety of credit products…it is possible that BNPL is a net positive for these consumers, even as they struggle to manage their debt load.”; and (3) my experience as someone who grew up in a low-income area in South Chicago is that people tend to manage their cash flows very tightly when they have low income and when they experience liquidity shortages, the lender of last resort ends up being family members and that can be very consequential. Lending regulations in the US are very pro-consumer compared to other countries and have many great protections for when people, unfortunately, aren’t able to make repayments. It’s important to understand that financial hardship happens to a lot of people and it’s all about what tools they’re offered to get themselves out of that situation9.

Alex Johnson from Fintech Takes wrote “Unlocking the Next Wave of Innovation” and emphasizes that embedded lending is the future. I very much agree with him. He also highlights the challenges for lending and focuses heavily on servicing and he is spot on.

Packy McCormick wrote "Attention is All You Need" and discussed the history of the algorithm and the paper that led to GPT. It’s really quite a fun read.

Patrick McKenzie wrote “Banking in very uncertain times.” It’s excellent. Please read and learn an extraordinary amount in ~7500 words.

Postscript

Did you like this post? Do you have any feedback? Do you have some topics you’d like me to write about? Do you have any ideas how I could make this better? I’d love your feedback!

Feel free to respond to this email or reach out to me on Twitter! 🤠

It was originally Henri Poincaré, the mathematician and physicist, who discovered Chaos in the 1880s while studying the three body problem (the problem of taking the initial positions and velocities of three point masses and solving for their subsequent motion according to Newton's laws of motion and law of universal gravitation) but Lorenz is attributed with what we call modern Chaos Theory.

An added benefit is the reduction in subjective human decision making, which is terribly ridden with bias. Purely relying on data certainly doesn’t fully eliminate bias but it helps you get started.

In my first post titled “Hello World” I referenced a quote from Shane Parrish about entropy, which said “we can define entropy as a measure of the disorder of the universe, on both a macro and a microscopic level” and I wrote about why I chose the title for this newsletter. “Why ‘Chaos Engineering’? Because the modern world is chaos and engineers make their best attempts to impose structure on a chaotic world sprinting towards entropy and I find that wildly entertaining.” I was mostly referring to my experience writing software for underwriting, so I’ve waited a long time to finally get to execute this pun and I’m happy to finally do it.

By the way, most rules engines are variants of the RETE algorithm developed by computer scientist Charles Forgy whose company, Rules Power, was acquired by FICO in 2005.

I say this explicitly for the few who may think this is helpful but most probably don’t need this level of bluntness.

After this post, I suppose, I should abuse the word “chaos” less. Probably not though.

This is still the code.

Looking at you, Hindenburg.

Of course, there are broader societal and policy failures at play since Health Care is the primary driver of bankruptcy.

Thanks for this, interesting for us at indó Iceland since we will soon start a buy or build discussion on a credit rules engine