Fintech Reckoning

On the future of finance and technology

Everything was beautiful and nothing hurt.

—Kurt Vonnegut, Slaughterhouse Five

Let us bow our heads and pray for all of the lost enterprise value in 2021. Amen. 🥲

Fintech was Glorious

Let’s pretend for a moment that we’re back in 2020 and that the world and financial markets were not doused in kerosene and burning in chaos.

Wasn’t it nice?

Public and private markets were drooling over Fintech companies and it seemed like liquidity events were happening left and right

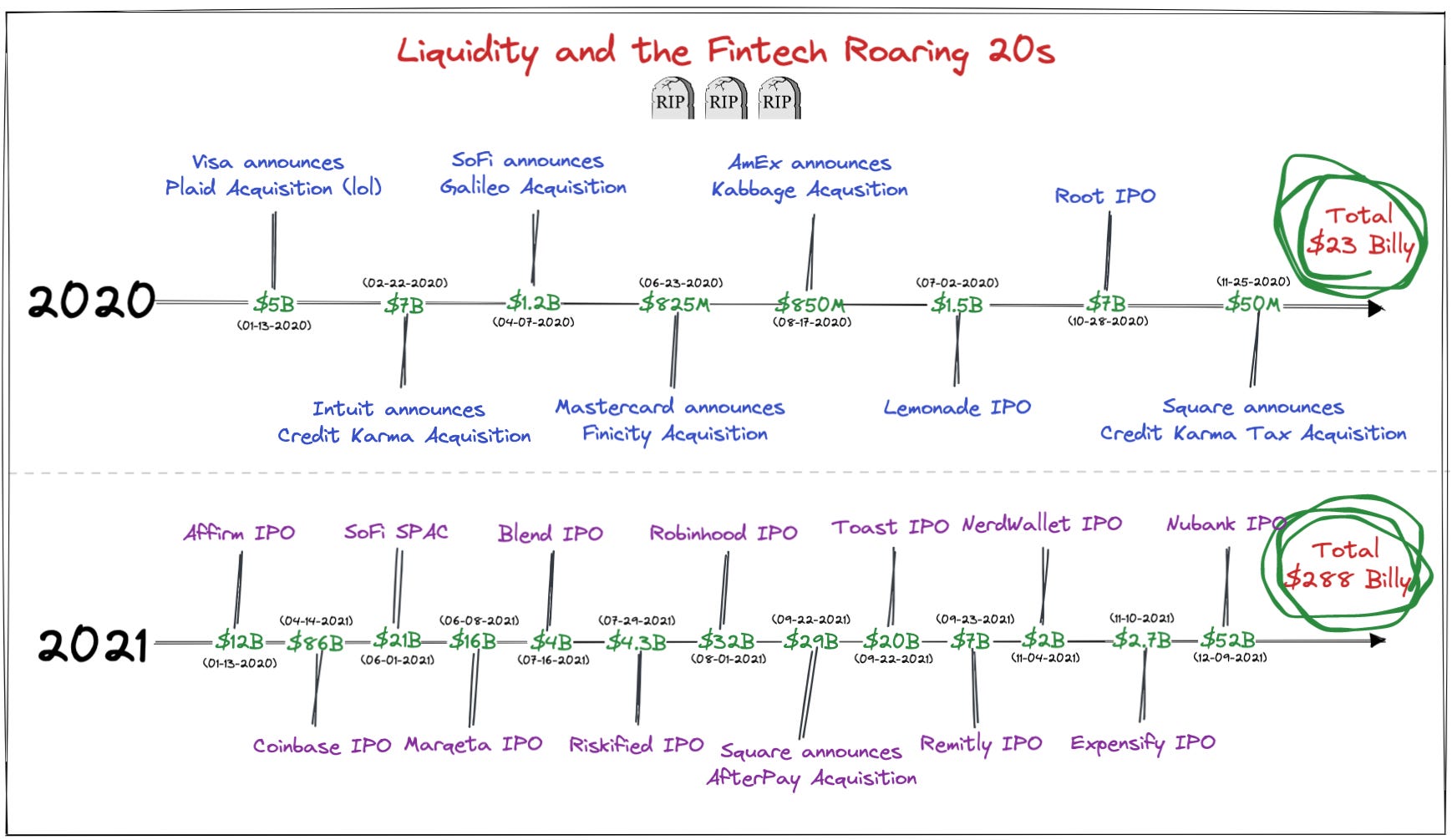

Reflecting on the timeline of events, it all really started when Visa tried to acquire Plaid for $5 billion.

After that things kind of got out of hand. In fact, in 2020 there were 2 Fintech IPOs and 6 acquisitions that amounted to $23 billion dollars and in 2021 there were 12 IPOs and 1 acquisition that amounted to $289 billion. 🤯

The Good Times are Over

But all good things come to an end and that end came roughly in January of 2022, basically the peak of the market.

Since then there’s been nothing but doom and gloom in the media1, whether it be layoffs at public companies or early stage companies shutting down entirely2—the news has almost exclusively been bad. Even this past week Goldman Sachs (my former employer) is allegedly reducing their consumer banking division3.

As the Federal Reserve gives priority to its inflation mandate, the increases in the federal funds rate has played a large role in the decimation of public markets but uncertainty across the global economy, lagging supply chain issues, expectations about tightened consumer spending, and the war in Ukraine has fueled that fear further.

The increases in interest rates have had a particularly significant impact on Fintech, largely because it impacts the cost of funds for lenders and puts additional pressure on margins, but the market has somehow forgotten that great lending and financial companies have been built during downturns before with much higher interest rates (e.g., Capital One started in 1994 and Discover in 1985).

Beyond the impact of rising rates, the CFPB has also turned up the heat on many Fintech companies. This certainly hasn’t helped the situation but overall I think it’s absolutely great! The CFPB was established to protect consumers and so long as they continue to honor that mandate the industry will be better off in the long term…that is, so long as they make sure to call out the real predatory actors.

Additionally, the OCC’s recent “Bank Supervision Operating Plan for Fiscal Year 2023” release highlights the importance that legal and compliance plays in Fintech, which along with the CFPB probably makes investors hesitant to make bets in such a highly regulated industry. I disagree with this personally but I think it may contribute to investor angst.

When will the pain end?

Who knows…probably the Federal Reserve.

I’m not a macroeconomist4 but I do think that the Federal Reserve is well equipped to get inflation under control5 and still prevent an entire economic collapse, even if most of the media would tell you otherwise. The good news is that capitalism moves quickly and the Fed can cut rates (i.e., incentivize growth) once inflation has tampered down to more regular levels (though I would expect more modest adjustments if that were the case).

As you may recall, the Federal Reserve has a dual mandate of maximizing employment and stabilizing prices. We’ve been at full employment roughly since August of 2021 and even as rates have increased we've continued to see a strong labor market, so I don't think the outlook really is as bad as many say—public markets are a different story and it's worth emphasizing that stocks aren't the economy (though an important piece of it).

Even so the IMF has forecasted significant slow downs in the global economy and the FOMC projects Real US GDP to be roughly 1% in 2023 and 1.7% in 2024, which is lower than their target of 2% - 3% in stable times. So the outlook isn’t exciting but it certainly is not a global meltdown.

Surviving

As the economy goes into a cooling state and markets continue to overreact, the most important thing for startups and Fintech companies to do is survive, obviously. While 2020 was a hot year for acquisitions, I suspect that we’ll see banks aggressively using their balance sheet to go shopping, so acquisitions will likely continue but expect much lower valuations.

Given the current market preferences, survival for public companies will only happen through profitability and actually adding value to your customers. So the question is who will weather the economic storm?

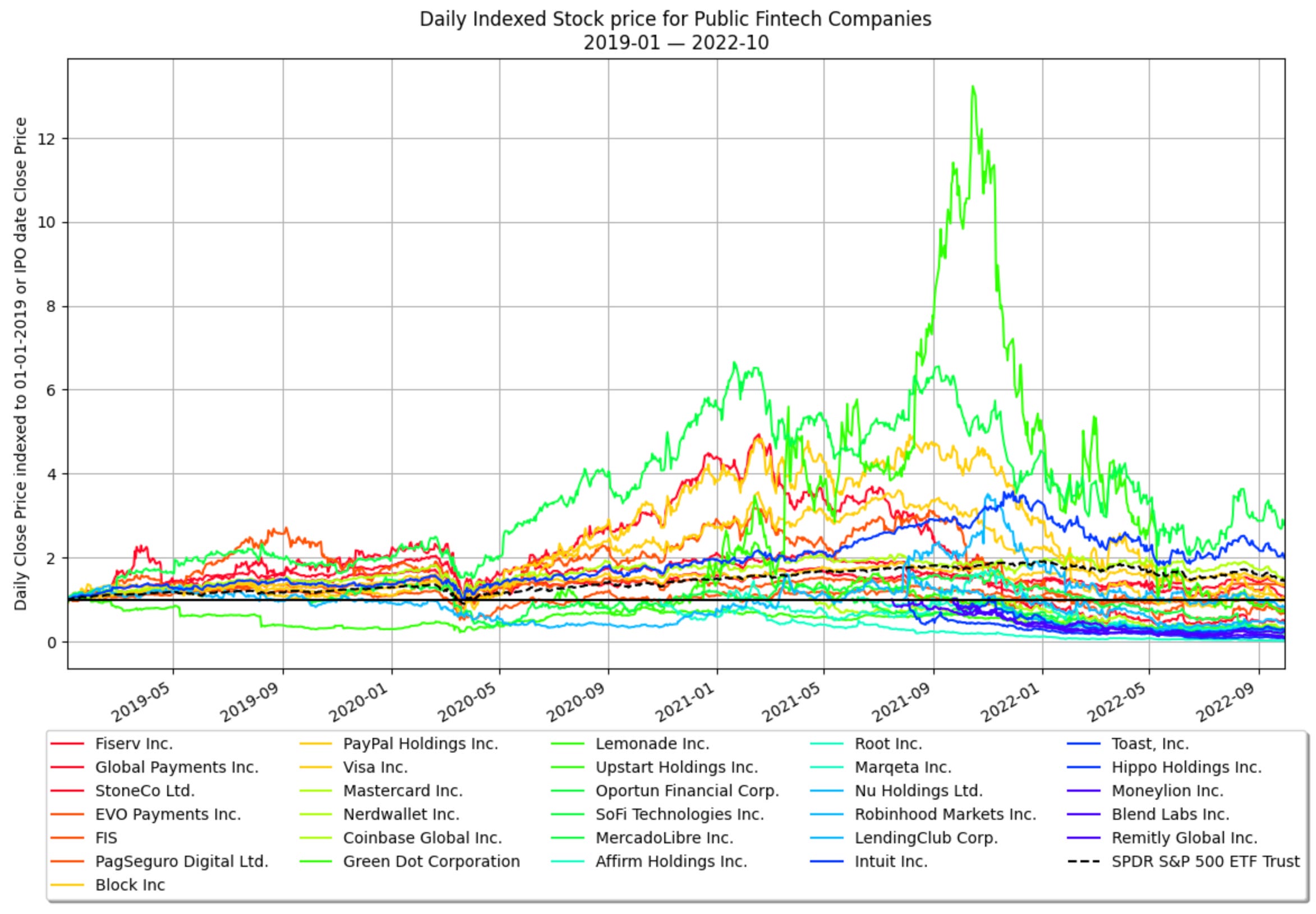

I decided to take a look at the data around public Fintech companies before the massive hype and bust cycle and it’s quite interesting to see current market preferences.

In short, it likes payments and hates everything else (except for Intuit???). Obviously the original market cap and valuation multiples in the early 2020s were unsustainable but to think that these businesses are worth less than they were two years ago seems kind of dumb6.

But, as you know:

The market can price irrationally longer than you can stay solvent. 😉

-A. Gary Shilling (mostly)

Beyond surviving, it’s actually a great time to launch a Fintech, great lending businesses are built during downturns. It’s easy to underwrite when delinquencies are low across the industry, but now is where differentiation happens. And it’s important to note that while increasing rates provides margin pressure, demand for lending increases so I believe many fintech companies will flourish during this time—so long as they add real value to their customers and manage risk vigilantly.

But where I am less optimistic is in international markets. As the dollar grows stronger international investments become harder to rationalize (from a US perspective). That and the fact that the Federal Reserve will probably not give much attention to countries outside of the US makes me rather bearish, so I expect things will be challenging for the coming years.

The Future of Fintech

Things will get worse before they get better in public and private markets.

Private markets began cooling valuations for fintech companies but early stage investing in Fintech gained a lot of momentum over the last couple of years, which means that for those that adapt and survive, we will begin seeing the fruits of their labor in the coming years.

Somewhat ironically, an unprecedented set of dry powder means that there’s capital to be deployed and eventually venture capitalist will place their bets on their favorite Fintech companies, which will further drive innovation in the coming years.

The Fintech companies that stunned the world in the early 2020s were built quietly with extraordinary effort during the previous decade when Fintech was boring. If investors and public markets find Fintech boring again so be it…the world still runs on money so innovation will happen regardless, it’s all a question of which investors will have the conviction to wait and which companies will continue to build meaningful products.

Lastly, as an engineer, my strong opinion is that the underlying technology on which Financial institutions and companies were built has changed. In the last ten years open source software, distributed computing, cryptography, analytics, big data, machine learning, and even programming languages themselves have dramatically improved how these institutions provide goods and services (i.e., value) to their customers and we are just getting started.

So my advice is simple: don’t look at your portfolio and just keep building. The future of finance depends on it.

Happy building. 👷♂️

-Francisco

Some Recommended Readings

Jason Mikula’s recent data deep dive on the Financial Health Network’s Financial Health Pulse is an incredible review on the unfortunate decline in Americans’ financial health.

This Week in Fintech’s Sophie Vo released a Q3’22 Macroeconomic Vibe Check and gave an extraordinary overview of the funding environment.

Alex Johnson’s The Fintech Factor is a wonderful review of what it was like building Fintech in the old days and it’s important history to understand how new companies will aim to compete in the new environment.

I really loved Simon Taylor’s “Who can win at Fintech in this market?”, which largely inspired me to write this article.

Macroeconomist Claudia Sahm recorded an incredible video on “Five Facts about Inflation” from a talk she gave at the Institute for Macroeconomic Policy where she gave an overview of the supply-side challenges contributing to inflation.

Adam Shapiro, VP of the San Francisco Federal Reserve, published a wonderful Letter decomposing inflation and showing that more than half of the current inflation is driven by supply constraints. This may suggest that federal reserve rate hikes (which target demand side) may not be able to fully address inflation.

Postscript

Did you like this post? Do you have any feedback? Do you have some topics you’d like me to write about? Do you have any ideas how I could make this better? I’d love your feedback!

Feel free to respond to this email or reach out to me on Twitter!

Sensationalist click-bait paints a misleading picture. Be careful what you read! 😉

RIP Fast 🫠

I will probably share my thoughts on this later. 😇

I was trained as a microeconomist but that doesn’t mean I can’t have opinions!

Even if the most recent inflation report means further pain, it’s worth noting that changes in interest rates don’t impact everything immediately.

Of course this may be an overstate as business fundamentals beyond growth are important but I think you get what I mean.